-1.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

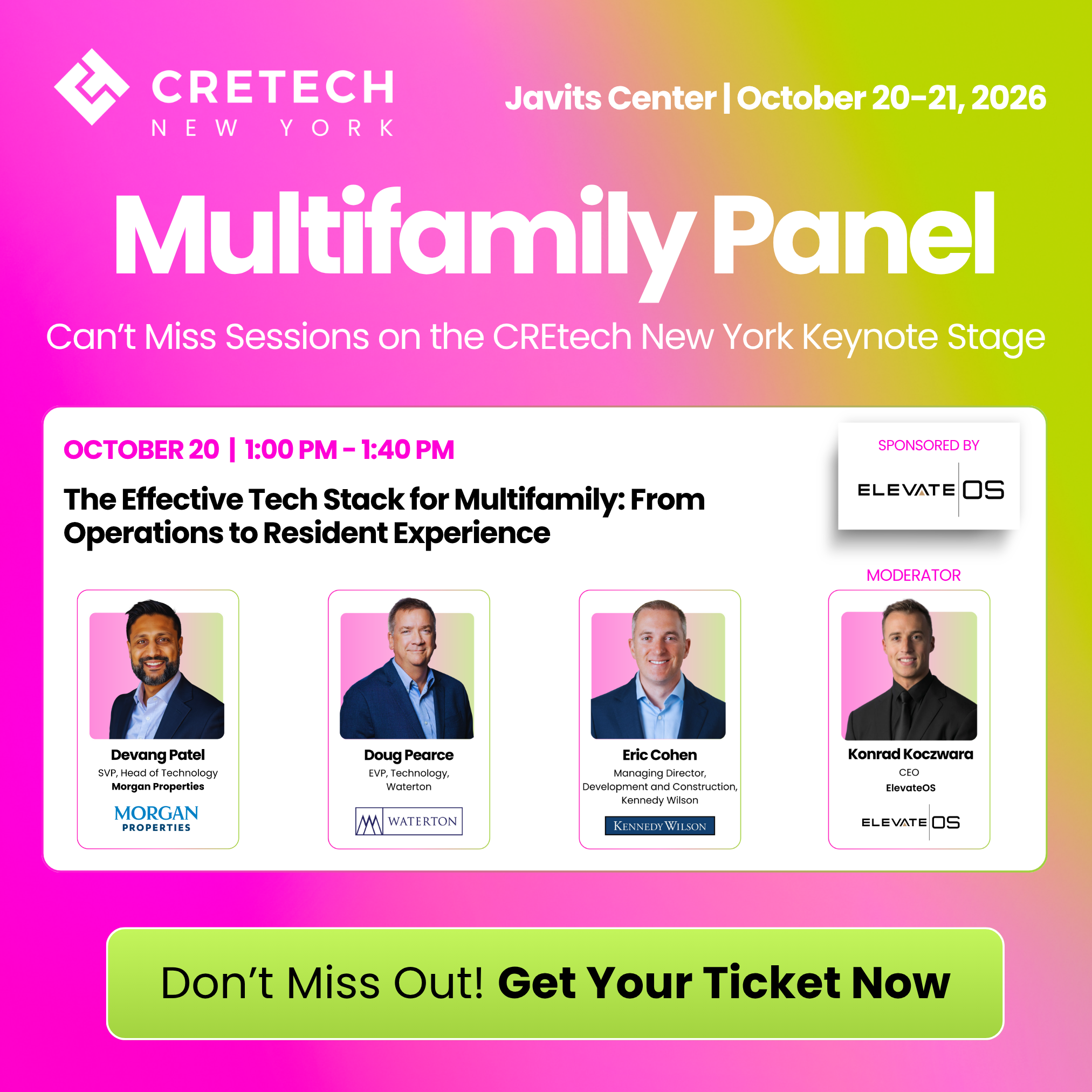

New York, NY — June 30, 2026 — CREtech, the world’s leading community of professionals devoted to...

New York, NY — June 30, 2026 — CREtech, the world’s leading community of professionals devoted to...